Long before I went to grad school, I worked for a construction company that specialized in building water and wastewater treatment plants. They got work by submitting bids. That’s how I got interested in auctions and I eventually wrote my dissertation on auctions. Since Swiss has been beating the drum for content, I thought I’d write a little about auctions. I’m not going to the write out the proofs this time because writing equations in Word makes me cranky.

Economists separate auctions into private value and common value auctions. The difference is driven by how the object for sale is valued. In a private value auction, there is no true, objective value. The value of the item for sale depends on the individual. In a common value auction, there is a true value that is the same to everyone and it doesn’t depend on the individual.

For a private value auction, consider a painting by an unknown artist. I think it’s beautiful and you think it’s ugly. The value depends on our private opinions – my value does not affect your value. For a common value auction, consider an oil lease. The amount of oil under the ground doesn’t change depending on who owns it.

First, I’ll talk about private value auctions. What is neat about private value auctions, is that as long as you meet certain criteria, the format doesn’t matter, they all raise the same revenue for a given number of bidders. This is known as the revenue equivalence theorem. (And thus, the bidders get the same surplus (profit) defined as the difference between the winner’s value and the price paid.)

What I mean by format, is the auction rules. A first price sealed bid is like a silent auction at a charity event. Bids are written down and submitted. They are opened and the high bidder wins and pays their own bid. A first price descending auction uses a clock. Bidders watch the clock count down and the first bidder to stop the clock gets the item and pays their own bid. This is also called a Dutch auction because the Dutch flower auctions use this mechanism.

A sealed bid second price auction (or Vickrey auction) is like a first price sealed bid auction in that the high bidder wins, but the winning bidder pays the second highest bid. I’m not aware of second price sealed bid auctions used in the wild. Vickrey developed it as it allows economists to investigate various aspects of behavior. A second price ascending auction (English) auction can be an open outcry auction like eBay or the type that Sloopy runs or even an ascending clock auction (Japanese auction). In these auctions, the high bidder wins and pays the winning bid, but it is equivalent to paying the second highest bid. It is easiest to see the equivalence if you think about an ascending clock auction. The price rises and the bidders drop as it reaches their values. The winner is the last one standing and pays the price at which the last bidder dropped out – equivalent to the second highest bid.

Auctions can be used to model other phenomena as well. In an all pay auction the high bidder wins, but all the bidders pay their own bids. This model is often used to analyze things like lobbying. And yes, this format will yield the same revenue as a first price sealed bid auction.

The criteria for revenue equivalence are:

- The bidders are risk neutral

- The values are independently and identically distributed

- the bidder with the highest value (and thus bid) wins (bids are monotonically increasing in value)

- the lowest value has an expected surplus of zero.

Now, revenue equivalence doesn’t mean strategically equivalent. People bid differently under the different formats. The first price sealed bid and the Dutch auction are strategically equivalent (bidders follow the same strategy), and the second price sealed bid and the English auction are strategically equivalent in the private value setting.

In the first price sealed bid auction and the Dutch auction, since winners pay their own bid, they don’t want to bid their actual value. If they did, they wouldn’t have any surplus. Instead, they bid slightly less than their value. How much less is determined by the number of bidders. As the number of bidders increases, they bid closer and closer to their own value. Their actual values are not revealed in the auction process.

The second price auction (whether sealed bid or ascending) is what economists and game theorists call a truth telling mechanism. In many economic transactions, it is in the interest of the parties to conceal information. If I let the car salesman know my top number, he will do all he can to get me to pay that amount. I’m sure you can all think of other examples. Second price private value auctions are truth telling mechanisms because it is your interest to bid your actual value. If you were to bid more than your value, you run the risk than the second highest bid is also above your actual value and instead of a surplus, you have a loss. If you bid less than your value, you run the risk that the high bid is above your bid, but less than your value, and thus you have lost the item and the surplus. So, the best strategy is to just bid your value, revealing the value in the process.

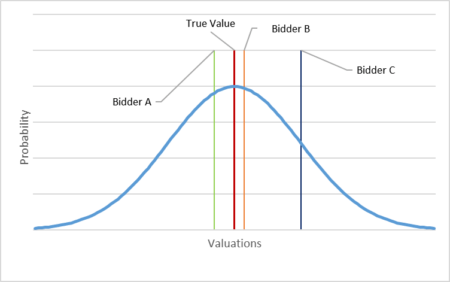

Next, let’s consider common value auctions. Common value auctions have some interesting effects. Most famously, common value auctions are subject to the winner’s curse. By winner’s curse, I mean winning is bad news. The phenomenon was first reported by oil companies. Here’s what’s happening:

Imagine we have three oil companies bidding on an oil lease in a first price sealed bid auction. The bidders have examined the lease and taken readings (Hi Agent Sloper!). Based on the readings they have an estimate of the true value and place their bids based on those estimates. Assuming bids are monotonically increasing in the estimates, Bidder C wins and learns that the other bidders think the true value is lower than Bidder C’s estimate. Oops.

In a common value setting, there is no revenue equivalence across auction formats. A first price sealed bid auction does not yield the same revenue as a second price sealed bid auction. The strategic equivalences I mentioned above do not necessarily hold either. While a first price sealed bid auction is still the same as a Dutch auction, a second price sealed bid auction and an ascending auction are not strategically equivalent. This is because in an ascending auction I can learn more about your estimate, which lets me refine my own bid. However, the second price sealed bid auction is still a truth telling mechanism.

Let’s try an example called the envelope game that I often used in class. I have two envelopes and I put some money into each envelope. Next, I show the contents of one envelope to Player A (call it $X) and the contents of the second envelope to Player B (call it $Y). The two players will bid for the two envelopes in a second price sealed bid auction. The winner gets both envelopes ($X+$Y) and pays me the second bid.

What should be Player A’s bid? What should be Player B’s bid? Post your answers in the comments and I’ll put the answer in the comments after about an hour.

In a common value auction, there is a true value that is the same to everyone and it doesn’t depend on the individual.

This jumped out to me. Value is subjective. Value always depends on the individual.

Let me finish reading.

For a common value auction, consider an oil lease. The amount of oil under the ground doesn’t change depending on who owns it.

Ahh. OK. I think I see what they’re getting at, but that really isn’t value. Owners will value the oil, regardless of amount, differently because value is subjective.

Not really – the oil has a market value which will vary, but it will be the same to the bidders.

But the bidders all have different fixed costs that only they know.

But it’s a commodity and they sell at market value. That affects profit not the value

Costs affect profit not markt value

Which I understand. It reminds me of Adam Smith and his dwelling on costs driving price. I understand a manufacturer (or someone in a similar position like an oil company) wants to sell for more than their costs. That doesn’t mean they have a buyer at that price since value is subjective.

Yes, but market value can be thought of as exogenous in this case because commodity ==> implies price takers

Now do military contract bidding.

The US military used to get some amazing equipment and tech via contract bids but all the waste and subsidizing really hides the actual cost of military assets.

I rate this article a 2 out of 10. Not even one explosion. What is with you people and writing about things without explosions?

Explosions will come when Tulip reads the comments.

And she’s trying to get me to do algebra.

Earn those cookies!

“I rate this article a 2 out of 10. Not even one explosion.”

And no sex! How am I supposed to masturbate to this?

We have faith.

Let’s try an example called the envelope game that I often used in class. I have two envelopes and I put some money into each envelope. Next, I show the contents of one envelope to Player A (call it $X) and the contents of the second envelope to Player B (call it $Y). The two players will bid for the two envelopes in a second price sealed bid auction. The winner gets both envelopes ($X+$Y) and pays me the second bid.

What should be Player A’s bid? What should be Player B’s bid? Post your answers in the comments and I’ll put the answer in the comments after about an hour.

I’ve been drinking a bit too much to do Game Theory and math, but I’ll take a stab.

A bids X, B bids Y.

A should bid п, and b should bid i+1.

Interesting article Tulip. I bought a used Prius at an online auction this year. My wife and I agreed $1500 was the highest we should go. The bidding goes up by $25 increments and as the end time came close it was over $1400. We said we’ll just put in our max bid of $1500 and see what happens and we ended up buying it for $1500. Another $25 would have won it for someone else. And it’s not a hard end time. If someone bids in the last 10 minutes then the time is extended, so the bidding continues until everyone else declines to bid again. Not sure what that would be labeled.

https://bid.repocast.com/lots/2870740#YXVjdGlvbltzdGF0dXNdPXBhc3QmaWQ9Mjg3MDc0MCZsaW1pdD0zMCZsb3Rba2V5d29yZHNdPTIwMDggVG95b3RhIFByaXVzJmxvdFttaWxlX3JhZGl1c109MjUmbG90W3N0YXRlXT1hbGwmbG90W3N0YXR1c109YWxsJm9mZnNldD00JnBhZ2U9MSZwcmV2W3BhZ2VdPWwmcHJldlt3aWRdPTI.

Still a second price auction, but these rules have been of interest.

See: https://www.jstor.org/stable/4135262?casa_token=i2OlXT_OuPwAAAAA%3A4m1k3KUHLP3rAqqNXurLLQvTbmLnLV3uhNI9KZNQFH9eI82XfY494kwwrp0ggtnr3bN5wFLawWVMTxp2e-9yOTvYRfIgrY00Ed2SJjrKz_8agEmMlnrH&seq=1#metadata_info_tab_contents

And: https://www.aeaweb.org/articles?id=10.1257/00028280260344632

I read every word of the article and I understood it! Yay! But not enough to try to solve the problem.

I used to do eBay auctions all the time before eBay got greedy.

My biggest problem with selling things is that I’m not aware of going rates, which is why when I DO use eBay, I always choose the auction format (with reserve) and not the “buy it now” format. The bidders do my homework for me. Frx, one time I sold off some of my old cross stitch patterns by a popular designer. Five patterns made my mortgage that month. ONE pattern went for almost $500. I would have had no idea because a) I didn’t know thye were out of print and b) didn’t really remember how old they were.

Now, selling things and haggling, which I also do, is a different proposition.

Thanks Mojeaux! I’m really glad it made sense, I wanted it to be accessible.

Well, okay, I’ll take a stab at the problem, but that’s not saying much.

IF IT WERE ME…

In a second-price sealed bid, if I’m person A, I’m going to bid X+1. If I’m person B, I’m going to bid Y+1.

#notme

You mention haggling… auctions seem to me to be haggling and I can’t stand that.

I like low-key haggling. I know what I will accept for an item, so for me, if the person goes, “Oh, okay,” then I get more than what I wanted. If the person goes, “Will you take X?” and I say, “No, $Y is firm,” then they either will or won’t buy it. All the same to me, since someone else will want it too.

When I sold my Granny car, I decided to sell it for $500. My husband and mom both thought there was no way I’d get that. I had 150 responses to my ad within a few hours. It was then I realized I could have gotten more. The first guy who showed up the next day (early on a Sunday morning, having driven 50 miles for it) got it.

It always pays to make sure you’re the guy who can walk away from the negotiation table.

It’s not haggling, because you’re competing with other people in the bid process. Haggling only occurs when there’s one seller and one buyer.

Yeah. Still rubs me the wrong way. I want a price to accept or reject.

My people skills kind of suck, FWIW.

Haggling is for situations where the value of people’s time is lower than the amount of a discount you can get.

In poorer places, haggling is more prevalent because people’s time isn’t worth much relative to most items forsale. In wealthier places, fixed prices usually prevail because haggling sellers elicit your reaction – “I’ve got better uses for my time than quibbling with you.”

In the U.S., haggling is usually reserved for big ticket items like houses or cars, where the asking versus selling price can be hundreds or thousands of dollars, but not every day stuff like groceries.

I was told there would be no math.

I’m assuming there is an amount greater than zero in each.

It’s also the reason I hated the many credit hours of Econ that I was required to take. Only thing worse was cost accounting…. Econ is preferable to cost accounting.

I used to be an ebay junkie. I would set sniper bots to bid at the last 3 seconds. PayPal has screwed that up for me.

My stepdad is a farm machinery auction junkie. The football field sized pole barn we built (and I nearly fell off the roof of) is full. I mean he has tractors with loader buckets raised to fit above the hay wagon in front of it FULL. Yet he still goes to auctions.

He’ll be rich after the zombie apocalypse.

Then again, how many people do you know that can hold an oat threshing party in this day and age.

Snipers have saved me from many an unnecessary purchase. I still hate them.

I don’t auction buy much on eBay anymore.

Most people round in their maximum prices so make your high bid the next bid increment up. So bid $51 and not $50.

My usual bid was $50.03. Those 3 cents won me several auctions.

I don’t buy much on ebay anymore either. The deals aren’t there.

Yes, I do that too, but you can’t beat a sniper.

I’m a gun auction junkie.

I always just set the maximum amt I was willing to pay and walked away.

Me thinks you will need Sloopy’s services when your dad passes on.

Your stepdad is Machinery Pete?

Uh, is pi part of the answer?

Mmmm, pie.

My head hurts now.

A = X +.75X (for Y)

B= Y + .75Y (for X)

Player A bids 2X and Player B bids 2Y. Then, if X is greater than Y, 2Y is less than X+Y. This is the Nash equilibrium, so DEG was close. However, his wasn’t an equilibrium because bidding X+1 would win if Player B bid Y.

This is the Nash equilibrium, so DEG was close.

So… I should post when I’m drunker than I am now?

😉

The answer is: Commissar C takes both envelopes, and throws Players A and B in a re-education camp for not paying their fair share (100%) to Czar Brandon.

I worked at an auction house for a couple years, even acted as the auctioneer once when the boss was late in his arrival, probably worked for an hour or so. It was a fun time but the ethics of some auctions are questionable. I’m not saying we were but there was an occasional mystery buyer or a phone bid. It’s a lot more fun when there is a big crowd and have 2-3 people working the crowd, which is not dishonest.

Private parties generally were willing to bid higher, dealers had to keep in mind their costs and a profit.

The Barrett-Jackson car auctions are enjoyable, they waste no time when the bidding slows, some cars seem to go for a very fair price.

The thing with high end auctions like that is they knowingly shill when nobody is in the room to try to start the bidding or move it along.

Cracks me up.

Enjoyable article, Riven, we generally don’t realize there is some science involved. Thanks

I’m too drunk, stoned and stupid to comment on this article… Happy Turkey Day, Tulip! Love ya!

…fades into the void…

Based on the readings they have an estimate of the true value and place their bids based on those estimates. Assuming bids are monotonically increasing in the estimates, Bidder C wins and learns that the other bidders think the true value is lower than Bidder C’s estimate. Oops.

This only applies in setting where what’s being auctioned has a true value for all bidders. In a lot of auctions, especially those I conduct, the actual value of the item varies by bidder.

(Ex: bidder 1 has a job that needs two D8-equivalent size dozers and he has one in his current fleet. The job generates $10,000 in revenue daily and the rental of a D8 is $10,000/week

Bidder 2 has a similar job but has two D8s in his fleet.

Bidder 3 has no current jobs and is purchasing the item to rent to other users.

The D8 going across the block is worth more to bidder 1 in real money because he can outbid bidder two for $100,000 and the job is expected to last another 12 weeks and he can quickly resell (read: wholesale)it at that time for $80k to bidder 3 or someone else in the rental business who can return a profit after 4 months of renting it out-which probably means after owning it for 8 months if his fleet utilization is 50%.)

I get the theory behind the piece, but there’s definitely not a universal application.

The first part of the article covers the private value auctions. Only the second part discusses common value auctions.

What is neat about private value auctions, is that as long as you meet certain criteria, the format doesn’t matter, they all raise the same revenue for a given number of bidders. This is known as the revenue equivalence theorem. (And thus, the bidders get the same surplus (profit) defined as the difference between the winner’s value and the price paid.)

But the different formats don’t raise the same revenue for a given number of bidders. Some sealed bid auctions will raise substantially more than open bidding based on the number of participants (not to mention many auctioneers running sealed bid auctions won’t disclose how many people have registered or bid on an item), and some items with open bidding will raise more given a certain number of bidders and their immediate utility of the item being bid on.

That may also not apply to your stuff, instead your auctions may be what we call affiliated private value auctions which usually applies to things like construction projects. But those involve more difficult math and I’m not sure I can explain the theory without the math. But, in a nutshell, the values are affiliated in that the valuations are in a much more narrow window – so if one construction firm thinks the project is worth $8M, then you won’t find another that thinks it is worth only $2M or one that thinks it is $20M. They’ll all be within a band of say $7M to $9M.

The items I sell tend to fluctuate based on the utility a given item has for specific bidders. See the above example. A number of Bidder 3s will always exist and the floor will always be set by those guys, because there are enough of them willing to purchase and sit on inventory. Bidder 1 and Bidder 2 usually exist in varying numbers so an item may have immediate utility for 3 Bidder 1s in a sale in June but there may only be 1 of them in a July sale, so the item has an immediate value of (at least) two bid increments more in June than it does in July, assuming you have at least one Bidder 2 in each auction.

I just won an item from the William Shatner Horse Charity Auction, so this is good timing! There were lots of items so it spread out a lot between the truly collectible items and just some things he signed. I went with one of the latter, since my interest was just to get an autograph since, well, it’s not likely I’ll be able to attend a con where he’s featured any time soon to get one myself, and he’s 90 years old.

A number of years ago I played in the BSG auctions to sell off the show memorabilia and one of those was live up in Hollywood. HOLY SHIT, is that a whole different feel, than doing online auctions. I had no idea til I was there, and I had to practically sit on my hands because it gets too exciting and you forget how much you were really willing to pay. But such great fun, too.

I thought he didn’t do autographs at all?

He may not (and possibly because of the charity auction), though I know he’ll do photo ops at some cons. So I’m happy I have my little mini poster signed!

I should say so! That’s a rare thing indeed.

I am a wimp at negotiations. Mrs. Hobbit, however, is ruthless. She could negotiate the devil out of his horns. I’ve learned to lean back and let her deal.

Also, thanks for the article. I have always assumed that an auction is the simplest version of laissez-faire capitalism, but I see that (as usual) it is much more complex than I thought.

Thx Tulip. Once again the place opens up insight into a world I know nothing about.

My only experience with auctions is equivalent to the What Would You Do if You Win the Lottery mind game. What would I bid on some cars at a Barrett-Jackson auction. IRL if I had enough FU/Jay Leno money? There’s almost no limit on what I might bid (which is why Jay doesn’t go to auctions and place the bids himself).

Thx Tulip. Once again the place opens up insight into a world I know nothing about.

What mikey said.

I’ve been to one auction. It was with my parents. They bid on several “collections” of mostly junk. I think they won some records they wanted.

This a good topic because I am considering divesting myself of all my unneeded possessions. I want to downsize and move very badly. I don’t know where to begin.

I understand New York became a bigger port in Colonial times than Philadelphia partly due to the Quaker merchants being opposed to haggling. They’d offer the importer what they thought was a fair price, take it or leave it so the importer had much less chance to bid up the sale price in a frenzied auction. But, at the end of the day, the Quaker merchant had to have been pretty shrewd, because the old joke is that “A Quaker can buy wholesale from a Jew and sell retail to a Scot, and still make a very nice profit.”

I think it was almost entirely because of the eerie canal.

Erie Canal was after colonial times.

My experience lately with auctions is from home consignment shops nearby(ish).

Two put a (usually) low fixed price on stuff, so if you want it and think it’s a great deal, you better buy it right away. Some stuff flies out the door, other stuff is overpriced and sits until the store tells the would be seller to take it back home.

The other place has a descending price auction, where they usually test market with a higher starting price and a floor at half the starting price. If we want something, we usually decide between the lowest price and the next to lowest price – and show up at opening time the day it hits our price point to see if it is still there.

https://archive.md/rDcbL/c969af35da3811a00b9d6c0012ced49015ed76fe.jpg

NSFW.

https://archive.md/4woFM/caf2554819d05b7703f1d09beb4009fbe3ff02ab.jpg

NSFW.

https://archive.md/okXSX/2df790a26f9108ff3aea3a5a38251a3bcbe193ac.jpg

NSFW.

https://archive.md/tygWq/bdc160e2189b7c039a2e92f6f8cc8b223e592acf.jpg

NSFW.

Not safe for wallet

Shooting at the walls of heartache bang, bang

I am the Firster

Well, I am the Firster

And heart to heart you’ll win

If you survive, the Firster, the Firster

I would have picked First is for Children.

In an effort to beat Ted’S to link the Bro’s mutilation of “The Warrior”, I found this in my sidebar.

I made it objectively better.

Interesting article Tulip.

Now a Thanksgiving feel good story for the group. (NO sarc)

https://dnyuz.com/2021/11/24/meat-is-hard-for-hungry-families-to-come-by-enter-these-deer-hunters/

If I miss any of you early sunrise time zones people because you have to deal with life before we wake up in the tropics. Have a great Thanksgiving!

“…deal with life before we wake up in the tropics.”

2 words for you. Just two.

Pearl. Harbor.

Ever hear of these White Stripes? I think they’re gonna make it, they’re really quite good

I heard of them First. I was in on it before you were even born, spittoon. Though I am probably the youngest here at Glibs.

Whatever’s in my envelope + 20%

Player A should offer 2*X and player B should offer 2*Y. That will be a Nash equilibrium.

Happy thanksgiving you all Glibs, hope it’s a good one. Always loved the Wednesday night before the holiday. Fun times.

Yesterday I heard this album from an electronic duo out of São Paulo and really dug it.

https://www.youtube.com/playlist?list=OLAK5uy_l2s-UNXr_ZuSG36_p6jMga4v6jEly3KrM

Nice music

Is it normal to get burned out on holidays as you get older?

I realized the other day that the only reason I really do anything for holidays (including my birthday) is that other people want me to and they’ll be upset if I don’t. Seems like with most of these days, you go through a bunch of effort and expense to make everything how it’s supposed to be on this one specific day, and when that day comes, it’s…. Okay. It’s just okay. Not substantially better than if I had just had dinner with family and friends, which can be done any day of the year. And it seems like no matter how hard I rack my brains to think of a perfect gift for someone, it’s never really a big hit. I can think of very few times that someone has genuinely enjoyed something I got them. But that’s the best I can do. It all feels like work. Just so much extra work.

… Dunno, maybe I’m just tired from prep-cooking Thanksgiving stuff and cranky because I ran out of beer and all the stores started closing at midnight at the start of the ‘Rona panic and never went back to 24 hours. I love all you crazy characters on this family-friendly site, and I hope you have a wonderful day tomorrow regardless of how you spend it or what cultural significance you ascribe to it.

“ Is it normal to get burned out on holidays as you get older?”

Hard to say. I think involvement with children in one’s life has a lot to do with the level of enjoyment and effort we put into celebrating holidays. For example, we like to commemorate children’s birthdays but we really don’t give a crap about our own, and even forget them utterly sometimes. (BTW, I think having a big birthday party for a 1 or 2 year old is silly; they’ll never remember it, so it’s for the parents really.)

Since my spouse and I don’t live near our 1st degree relatives anymore, we don’t make too much of a deal of thanksgiving, but it is a bright spot in the otherwise somewhat grim transition to winter. We make traditional dishes that remind us of our roots and our long-go e relatives.

Christmas is absolutely our favorite, but for the past 3 years it’s been minimal in our house. Partly because moving to California was tough and the house didn’t feel like “home” so much. Now that we’ve been in NV only for less than 2 months, we feel so at home we are planning to put up wreathes and lights after thanksgiving for Christmas. I love the fact that Christmas cheers the days that are otherwise dominated by short days and cold weather. No idea if I’d care about Christmas in Peru

So maybe some of caring less about holidays is a reflection of our connection to our families, our own pasts, and our community?

.

Well said. There are so many variables that affect one’s holiday “cheer”.

This is the first holiday season in 22 years without my daughter living with us. I honestly don’t want to do any decorating, because I don’t care about it anymore. I’ll do my usual though; take care of the non-tree and outside stuff. It’s not like she won’t be here for dinner today, or for Christmas, but the feeling is different. She actually was here last night to help my wife prep for today. My wife had to wake me up to say goodnight to her.

(BTW, I think having a big birthday party for a 1 or 2 year old is silly; they’ll never remember it, so it’s for the parents really.)

It’s like a party celebrating adulthood. “Look at us! We’re going to be responsible adults now.”

Three strikes and yer out? Enjoy Turkey Day, young lady!

Family can be a pain in the ass. Well, mine at least. “Forced” or obligatory holidays only make me defiant.

Tres Sr. isnt cooking, Tres Version 2.0 is with his mom’s family. Jugsy is home, I worked all night, and doge seems happy to have both his people around him.

Im happy to lay on the couch and not leave the house until work tonight.

Yup, for me at least. Stopped all of that nonsense about ten years ago. A day is like any other day to me. I’m too old to put up with forced merriment. Go ahead and do your own thing and I’ll do mine.

It’s one of the few things the Jehovah’s Witnesses, who don’t celebrate holidays, got right.

Spiccolli really sells that turtleneck, doesn’t he?

Still the best teen coming of age movie ever. I wonder what actors they’ll use when they remake it.

+2 Phoebe Cates’s t0ts

She could probably still play the weird biology teacher’s wife.

If your holidays don’t include celebratory naked time, you’re doing it wrong.

We do that at the dark of the moon, monthly. Invite the neighbors over, grill some ribs, frolic naked under the stars. You know, community!

Thanks Tulip. The auctions I usually participate in are always private value.

The key for me is finding something that nobody else realizes the value of. Which has become more difficult in the age of the Internet.

But isn’t that an ideal?

For the seller, yes.

suh’ fam

yo whats goody yo

TALL THANKSGIVING CANS!

Solved the furnace problem. That’s goody. So many niggling set-backs happening lately but I’m going to deal with them one at a time lest I become overwhelmed and fall into despair. New part is to be ordered tomorrow but I finessed the old one to hang in there for awhile yet. SHORT CANS SENSEI!

It was the thermostat. Be honest with us.

Ackchewally it is the control module which has been a little hinky for a couple of years. He don’t like wet, cold and windy. I just removed it, took out that little center screw and let it sit for awhile. Then I reinstalled it and played with the setting until the status indicators seemed close and fine tuned from there. It’s one of only two mechanical parts in the furnace and the fan runs fine. Yusef would have been proud of me!

A small victory but I’ll gladly accept this one!

Sounds like the shitty Rockwell® gas valve on my manic-depressive water heater. Which only seems to have issues staying lit when Jugsy is home.

It sends itself into any number of faults which wont clear unless I disconnect 1 wire and let it sit and think about its unacceptable behavior for about an hour.

Kinda like making it sit in the corner.

Yup. It just needed to air out a bit. Furnace is ten years old and I’ll admit to not changing filters to spec. It really doesn’t like our spring and early winter weather. We got 5 inches of wet snow and high winds yesterday.

Ha! Jugsy takes long, luxurious baths I’d assume? No wonder Rockwell gets cranky!

That and 2 weeks worth of laundry in an afternoon.

I figured it was because somebody was watching it.

I teed that up for someone. Much obliged, tEdS

If I was a smart cookie I think I would have enjoyed economics. Interesting article, Prof. Tulip.

Happy day, Americans.

The pandemic has stamped down what was my blooming Gunbroker “problem”. Back when there were deals to be had, I was much more inclined to bid. I’m not much for paying list or inflated prices.

Happy Thanksgiving, y’all!!

Its thanksgiving, and Im only going to say it another dozen times or two.

Why do native Americans hate snow?

Because it’s white and settles on their land.

Still “smirking funny”.

It’s like “How do you make a hormone?’

Dont pay her.

Never gets old so long as teenaged boys are underfoot. Like little girls and skipping cadences.

https://www.wfmz.com/news/area/lehighvalley/nazareth-area-school-district-makes-wearing-masks-in-classroom-optional/article_d3322a4e-4d6e-11ec-9271-f730de35c103.html

Good for them. Fuck Wolf.

https://www.fox5vegas.com/news/us_world_news/professor-who-wrote-about-adults-attracted-to-minors-resigns/article_a22d5c14-cd50-5da6-9521-73f8cc773782.html

I guess this means I support cancel culture. ?

I’m torn on this one to be honest. As a free speech absolutist I don’t like to see people get harassed into quitting or being fired for what they say or write. Then again, the normalization of certain proclivities needs to be nipped in the bud and once these kinds of people get their foot in the door they never ever stop.

Ok. I can get more on board support this these kind of people.

https://breaking911.com/ny-man-gets-30-years-for-coaching-wife-to-abuse-toddler-on-video-feds-say/

*supporting cancelling these…

Meh. You get the idea.

She really needs to line-up that wolf pussy on her lip.

Yeah, that’s terrible.

“Sorry not sorry.”

sheesh

As the Heir Apparent to the Drinkingest Glib, I declare that this Turkey Day shall be the most Joyous, Own The Libs At The Dinner Table event since 2016! Not really, have fun. Meet! Mingle! Spread the Koof!

Re-educate your crazy uncle!

“Teacher Says…” Oh God I’ve lived that.